424B3: Prospectus filed pursuant to Rule 424(b)(3)

Published on March 13, 2024

| PROSPECTUS SUPPLEMENT NO. 2 | Filed pursuant to Rule 424(b)(3) |

| (To prospectus dated September 25, 2023) | Registration No. 333-273183 |

NET POWER INC.

204,903,904 SHARES OF CLASS A COMMON STOCK

10,900,000 WARRANTS TO PURCHASE SHARES OF CLASS A COMMON STOCK

This prospectus supplement is being filed to update and supplement the information contained in the prospectus dated September 25, 2023 (the “Prospectus”), with the information contained in our Annual Report on Form 10-K filed with the Securities and Exchange Commission (the “SEC”) on March 11, 2024 (the “Annual Report”). Accordingly, we have attached the Annual Report to this prospectus supplement.

The Prospectus and this prospectus supplement relate to the resale from time to time of 204,903,904 shares of our Class A common stock, par value $0.0001 per share (the “Class A Common Stock”), by the selling security holders named in the Prospectus or their permitted transferees, which consist of (i) 54,044,995 shares of Class A Common Stock issued at a purchase price of $10.00 per share in a private placement that closed substantially concurrently with the consummation of the Merger (as defined in the Prospectus), (ii) 2,500 shares of Class A Common Stock issued to Rice Acquisition Sponsor II LLC (“Sponsor”) in a private placement prior to the consummation of the initial public offering (the “IPO”) of Rice Acquisition Corp. II (“RONI”), at an effective price of approximately $0.0036 per share, (iii) 10,900,000 shares of Class A Common Stock issuable upon exercise of the Private Placement Warrants (as defined below), originally acquired at a purchase price of $1.00 per warrant, (iv) 7,432,688 shares of Class A Common Stock issuable upon redemption of the 7,432,688 units of NET Power Operations LLC (f/k/a Rice Acquisition Holdings II LLC) (“Opco”) held by the initial shareholders of RONI or transferees thereof, all of which were issued prior to the consummation of the IPO at an effective price of approximately $0.0036 per unit, (v) 132,205,114 shares of Class A Common Stock issued or issuable upon redemption of the 132,205,114 units of Opco (“Opco Units”) issued as consideration upon consummation of the Merger to certain Legacy NET Power Selling Securityholders (as defined in the Prospectus) at a value of $10.00 per unit, and (vi) 318,607 shares of Class A Common Stock issuable upon the redemption of the 318,607 Opco Units issued to Baker Hughes Energy Services LLC (an affiliate of Baker Hughes Company) for services provided by Nuovo Pignone International, S.r.l. (an affiliate of Baker Hughes Company) pursuant to the Amended and Restated JDA (as defined in the Prospectus). In addition, the Prospectus and this prospectus supplement relates to the resale from time to time of the 10,900,000 warrants (the “Private Placement Warrants”) issued to Sponsor at a purchase price of $1.00 per warrant in a private placement that closed simultaneously with the consummation of the IPO. Each Private Placement Warrant is exercisable to purchase for $11.50 one share of Class A Common Stock, subject to adjustment.

This prospectus supplement updates and supplements the information in the Prospectus and is not complete without, and may not be delivered or utilized except in combination with, the Prospectus, including any other amendments or supplements thereto. This prospectus supplement should be read in conjunction with the Prospectus, and if there is any inconsistency between the information in the Prospectus and this prospectus supplement, you should rely on the information in this prospectus supplement. The information in this prospectus supplement modifies and supersedes, in part, the information in the Prospectus. Any information in the Prospectus that is modified or superseded shall not be deemed to constitute a part of the Prospectus except as modified or superseded by this prospectus supplement.

You should not assume that the information provided in this prospectus supplement or the Prospectus is accurate as of any date other than their respective dates. Neither the delivery of this prospectus supplement and Prospectus, nor any sale made hereunder, shall under any circumstances create any implication that there has been no change in our affairs since the date of this prospectus supplement or that the information contained in this prospectus supplement or the Prospectus is correct as of any time after the date of that information.

The Class A Common Stock and warrants initially sold as part of the units issued in the IPO (the “Public Warrants”) are listed on the New York Stock Exchange (the “NYSE”) under the symbols “NPWR” and “NPWR WS,” respectively. On March 12, 2024, the last sale price of the Class A Common Stock and the Public Warrants as reported on the NYSE were $9.00 per share and $1.90 per warrant, respectively.

Investing in our securities involves certain risks, including those that are described in the section titled “Risk Factors” beginning on page 8 of the Prospectus, as updated and supplemented by the section entitled “Risk Factors” included in the Annual Report (which is attached to this prospectus supplement).

Neither the SEC nor any state securities commission has approved or disapproved of the securities to be issued under the Prospectus or determined if the Prospectus or this prospectus supplement is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus supplement is March 13, 2024.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2023

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission file number 001-40503

NET Power Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 98-1580612 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

320 Roney St., Suite

200

Durham, North Carolina 27701

(Address of Principal Executive Offices)

Registrant’s telephone number, including area code: (919) 287-4750

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Class A Common Stock | NPWR | The New York Stock Exchange | ||

| Warrants, each exercisable

for one share of Class A Common Stock at a price of $11.50 |

NPWR-WT | The New York Stock Exchange |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the registrant’s voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2023 was approximately $271,915,748 (computed by reference to the last per share sale price of the Class A Common Stock on the New York Stock Exchange of $13.00 on such date).

The registrant had outstanding 71,960,052 shares of Class A Common Stock and 141,801,811 shares of Class B Common Stock as of March 7, 2024.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement for the registrant’s 2024 Annual Meeting of Stockholders have been incorporated by reference into Part III of this Report.

TABLE OF CONTENTS

i

Unless otherwise expressly stated or, unless the context otherwise requires, references in this Annual Report on Form 10-K (this “Report”) to:

| ● | “8 Rivers” means 8 Rivers Capital, LLC, a Delaware limited liability company (a company controlled by SK Energy); |

| ● | “Amended and Restated JDA” means the Amended and Restated Joint Development Agreement, dated December 13, 2022, by and among Old NET Power, RONI, RONI OpCo, NPI and NPT, as amended, supplemented or otherwise modified from time to time in accordance with its terms; |

| ● | “Baker Hughes” or “BH” means Baker Hughes Company, a Delaware corporation; |

| ● | “BHES” means Baker Hughes Energy Services LLC, a Delaware limited liability company and affiliate of Baker Hughes; |

| ● | “BHES JDA” means collectively, the Original JDA and the Amended and Restated JDA |

| ● | “Board” or “Board of Directors” means the board of directors of the Company; |

| ● | “Business Combination Agreement” means the Business Combination Agreement, dated as of December 13, 2022, by and among RONI, RONI OpCo, Buyer, Merger Sub and Old NET Power, as amended by the First Amendment to the Business Combination Agreement, dated as of April 23, 2023, by and between Buyer and Old NET Power; |

| ● | “Business Combination” means the Domestications, the Merger and other transactions contemplated by the Business Combination Agreement, collectively, including the PIPE Financing; |

| ● | “Buyer” means Topo Buyer Co, LLC, a Delaware limited liability company and a direct, wholly owned subsidiary of OpCo (following the Domestications) or of RONI OpCo (prior to the Domestications); |

| ● | “Class A Common Stock” means the Class A common stock, par value $0.0001 per share, of NET Power; |

| ● | “Class B Common Stock” means the Class B common stock, par value $0.0001 per share, of NET Power; |

| ● | “Clean,” in relation to the energy generated through the Net Power Cycle, refers to the NET Power Cycle’s capability to significantly reduce direct CO2 emissions and emissions of other air pollutants in comparison to energy generated with conventional gas-fired technology; |

| ● | “Closing” means the consummation of the Business Combination contemplated by the Business Combination Agreement; |

| ● | “Closing Date” means June 8, 2023, the date on which the Closing occurred; |

| ● | “Common Stock” means the Class A Common Stock and Class B Common Stock; |

| ● | “Company,” “our,” “we” or “us” means, prior to the Business Combination, RONI or Old NET Power, as the context suggests, and, following the Business Combination, NET Power Inc., in each case, with its consolidated subsidiaries; |

| ● | “Constellation” means Constellation Energy Generation, LLC, a Pennsylvania limited liability company formerly known as Exelon Generation Company, LLC; |

| ● | “Demonstration Plant” means the facility located in La Porte, Texas used to demonstrate the viability of the NET Power Cycle; |

| ● | “DOE” means the United States Department of Energy; |

| ● | “Domestication” means the change of RONI’s jurisdiction of registration by deregistering as a Cayman Islands exempted company and continuing and domesticating as a corporation registered under the laws of the State of Delaware, upon which RONI changed its name to NET Power Inc.; |

| ● | “Domestications” means the Domestication and the OpCo Domestication; |

| ● | “Exchange Act” means the Securities Exchange Act of 1934, as amended; |

ii

| ● | “Gen1U” means the Company’s first commercial-scale power plant; |

| ● | “IPO” means RONI’s initial public offering, which was consummated on June 18, 2021; |

| ● | “Legacy NET Power Holders” means the holders of equity securities of Old NET Power prior to the consummation of the Merger; |

| ● | “Merger” means the merger of Merger Sub with and into Old NET Power pursuant to the Business Combination Agreement, in which Old NET Power survived and became a direct, wholly owned subsidiary of Buyer; |

| ● | “Merger Sub” means Topo Merger Sub, LLC, a Delaware limited liability company and a direct, wholly owned subsidiary of Buyer; |

| ● | “NET Power” means NET Power Inc., a Delaware corporation (f/k/a Rice Acquisition Corp. II), with its consolidated subsidiaries (unless the context otherwise indicates), upon and after the Domestication; |

| ● | “NPI” means Nuovo Pignone International, S.r.l., an Italian limited liability company and affiliate of Baker Hughes; |

| ● | “NPT” means Nuovo Pignone Tecnologie S.r.l., an Italian limited liability company and affiliate of Baker Hughes; |

| ● | “NYSE” means the New York Stock Exchange; |

| ● | “Old NET Power” means, prior to the consummation of the Merger, NET Power, LLC, a Delaware limited liability company; |

| ● | “OpCo” means NET Power Operations LLC, a Delaware limited liability company (f/k/a Rice Acquisition Holdings II LLC), upon and after the OpCo Domestication; |

| ● | “OpCo Domestication” means the change of RONI OpCo’s jurisdiction of registration by deregistering as a Cayman Islands exempted company and continuing and domesticating as a limited liability company registered under the laws of the State of Delaware, upon which RONI OpCo changed its name to NET Power Operations LLC; |

| ● | “OpCo LLC Agreement” means the Second Amended and Restated Limited Liability Company Agreement of OpCo, dated as of June 8, 2023, which was entered into in connection with the Closing; |

| ● | “OpCo Unitholder” means a holder of OpCo Units; |

| ● | “OpCo Units” means the units of OpCo; |

| ● | “Original JDA” means the Joint Development Agreement, dated February 3, 2022, by and among Old NET Power, NPI and NPT, as amended by the First Amendment to Joint Development Agreement, dated effective June 30, 2022, by and among the same parties; |

| ● | “OXY” means OLCV NET Power, LLC, a Delaware limited liability company; |

| ● | “PIPE Financing” means the issuance and sale of 54,044,995 shares of Class A Common Stock for aggregate consideration of $540,449,950 in private placements pursuant to subscription agreements that RONI entered into with certain qualified institutional buyers and accredited investors, which was consummated immediately prior to the Merger; |

| ● | “PIPE Investors” means the investors who participated in the PIPE Financing; |

| ● | “Predecessor Period” means the period presented in the consolidated financial statements contained in this Report or the accompanying footnotes that relates to Predecessor, as defined and described in Note 3 to the consolidated financial statements contained in this Report; |

| ● | “Preferred Stock” means shares of NET Power preferred stock, par value $0.0001; |

| ● | “Principal Legacy NET Power Holders” means OXY, Constellation and 8 Rivers (through NPEH); |

| ● | “Private Placement Warrants” means the 10,900,000 warrants to purchase shares of Class A Common Stock that were issued and sold to Sponsor in a private placement in connection with the IPO; |

iii

| ● | “Public Warrants” means the warrants to purchase shares of Class A Common Stock that were issued and sold as part the units of RONI in the IPO; |

| ● | “RONI” means Rice Acquisition Corp. II, a Cayman Islands exempted company, prior to the Domestication; |

| ● | “RONI OpCo” means Rice Acquisition Holdings II LLC, a Cayman Islands limited liability company and direct subsidiary of RONI, prior to the Domestications; |

| ● | “SEC” means the U.S. Securities and Exchange Commission; |

| ● | “Securities Act” means the Securities Act of 1933, as amended; |

| ● | “Sponsor” means Rice Acquisition Sponsor II LLC, a Delaware limited liability company; |

| ● | “Successor Period” means the period presented in the consolidated financial statements contained in this Report or the accompany footnotes that relates to Successor, as defined and described in Note 3 to the consolidated financial statements contained in this Report; |

| ● | “Tax Receivable Agreement” or “TRA” means the Tax Receivable Agreement, dated June 8, 2023, entered into by NET Power and OpCo with OpCo Unitholders who received OpCo Units pursuant to the Business Combination Agreement as consideration for equity interests in Old NET Power and the Agent (as defined therein); |

| ● | “Up-C” means umbrella partnership, C corporation, which describes a corporate structure in which an ultimate c corporation parent consolidates a partnership or partnership structure treated as a pass-through entity for US state and federal purposes tax; |

| ● | “Warrant Agreement” means the Warrant Agreement, dated as of June 15, 2021, by and among RONI, RONI OpCo and Continental Stock Transfer & Trust Company as it may be amended and/or restated from time to time in accordance with its terms;and |

| ● | “Warrants” means, collectively, the Public Warrants and Private Placement Warrants. |

In addition, the following is a glossary of key industry terms used herein:

| ● | “CO2” means carbon dioxide; |

| ● | “CO2e” means the number of metric tons of CO2 emissions with the same global warming potential as on metric ton of another greenhouse gas |

| ● | “MW” means megawatt; |

| ● | “MWe” means megawatt electrical which refers to the electricity output capability of a plant; |

| ● | “MWth” means megawatt thermal which refers to the input energy required; |

| ● | “NOX” means nitrogen oxides; |

| ● | “sCO2” means supercritical carbon dioxide; and |

| ● | “SOX” means sulfur oxides. |

iv

Cautionary Note Regarding Forward-Looking Statements

This Report contains “forward-looking statements” within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. Statements that do not relate strictly to historical or current facts are forward-looking and usually identified by the use of words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “future,” “intend,” “may,” “opportunity,” “plan,” “project,” “seek,” “should,” “strategy,” “will,” “will likely result,” “would” and other similar words and expressions, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements may relate to the development of the Company’s technology, the anticipated demand for the Company’s technology and the markets in which the Company operates, the timing of the deployment of plant deliveries, and the Company’s business strategies, capital requirements, potential growth opportunities and expectations for future performance (financial or otherwise). Forward-looking statements are based on current expectations, estimates, projections, targets, opinions and/or beliefs of the Company, and such statements involve known and unknown risks, uncertainties and other factors.

The risks and uncertainties that could cause those actual results to differ materially from those expressed or implied by these forward-looking statements include, but are not limited to: (i) risks relating to the uncertainty of the projected financial information with respect to the Company and risks related to the Company’s ability to meet its projections; (ii) the ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition, the ability of the Company to grow and manage growth profitably and the ability of the Company retain its management and key employees; (iii) the Company’s ability to utilize its net operating loss and tax credit carryforwards effectively; (iv) the capital-intensive nature of the Company’s business model, which may require the Company to raise additional capital in the future; (v) barriers the Company may face in its attempts to deploy and commercialize its technology; (vi) the complexity of the machinery the Company relies on for its operations and development; (vii) the Company’s ability to establish and maintain supply relationships; (viii) risks related to the Company’s arrangements with third parties for the development, commercialization and deployment of technology associated with the Company’s technology; (ix) risks related to the Company’s other strategic investors and partners; (x) the Company’s ability to successfully commercialize its operations; (xi) the availability and cost of raw materials; (xii) the ability of the Company’s supply base to scale to meet the Company’s anticipated growth; (xiii) the Company’s ability to expand internationally; (xiv) the Company’s ability to update the design, construction and operations of its technology; (xv) the impact of potential delays in discovering manufacturing and construction issues; (xvi) the possibility of damage to the Company’s Texas facilities as a result of natural disasters; (xvii) the ability of commercial plants using the Company’s technology to efficiently provide net power output; (xviii) the Company’s ability to obtain and retain licenses; (xix) the Company’s ability to establish an initial commercial scale plant; (xx) the Company’s ability to license to large customers; (xxi) the Company’s ability to accurately estimate future commercial demand; (xxii) the Company’s ability to adapt to the rapidly evolving and competitive natural and renewable power industry; (xxiii) the Company’s ability to comply with all applicable laws and regulations; (xxiv) the impact of public perception of fossil fuel-derived energy on the Company’s business; (xxv) any political or other disruptions in gas producing nations; (xxvi) the Company’s ability to protect its intellectual property and the intellectual property it licenses; (xxvii) risks relating to data privacy and cybersecurity, including the potential for cyberattacks or security incidents that could disrupt our or our service providers’ operations; (xxviii) potential litigation that may be instituted against the Company; and (xxix) other risks and uncertainties indicated in Part I, Item 1A of this Report, and other documents subsequently filed with the SEC by the Company.

Should one or more of these risks or uncertainties materialize, or should any of the assumptions made by our management prove incorrect, actual results may vary in material respects from those projected in the forward-looking statements contained in this Report. Accordingly, you should not place undue reliance on these forward-looking statements in deciding whether to invest in our securities.

Forward-looking statements speak only as of the date they are made. Except to the extent required by applicable law or regulation, we undertake no obligation to update the forward-looking statements contained herein to reflect events or circumstances after the date of this Report or to reflect the occurrence of unanticipated events. The Company gives no assurance that it will achieve its expectations.

v

Summary Risk Factors

Our business is subject to numerous risks and uncertainties, including those highlighted in Item 1A, “Risk Factors,” that represent challenges that we face in connection with the successful implementation of our strategy and the growth of our business. In particular, the following risks, among others, may offset our competitive strengths or have a negative effect on our business strategy:

| ● | Old NET Power has incurred significant losses since inception, and we anticipate that we will continue to incur losses in the future, and we may not be able to achieve or maintain profitability. |

| ● | We may be unable to manage our future growth effectively. |

| ● | We face significant barriers in our attempts to deploy our technology and may not be able to successfully develop our technology. |

| ● | The technology we are developing will rely on complex machinery for its operation and deployment involves a significant degree of risk and uncertainty in terms of operational performance and costs. |

| ● | We, our partners or our third-party suppliers may experience delays in the development and manufacturing of turbo expanders, heat exchangers and other implementing technology. |

| ● | Suppliers of key equipment to our customers may not be able to scale to the production levels necessary to meet the anticipated growth in demand for our technology. |

| ● | We, our licensees, and our partners may not be able to establish supply relationships for necessary components or may be required to pay costs for components that are higher than anticipated. |

| ● | Our deployment plans rely on the development and supply of turbomachinery and process equipment by NPI pursuant to a joint development agreement. |

| ● | Our commercialization strategy relies heavily on our relationship with Baker Hughes, OXY, and other strategic investors and partners, who may have interests that diverge from ours and who may not be easily replaced if our relationships terminate. |

| ● | Our partners have not yet completed development of, and finalized schedules for, delivery of key process equipment to customers, and any setbacks we may experience during our first commercial delivery and other demonstration and commercial missions could have material adverse effects on our business, financial condition and results of operations and could harm our reputation. |

| ● | Manufacturing and transportation of key equipment may be dependent on open global supply chains. |

| ● | Manufacturing and construction issues not identified prior to design finalization, long-lead procurement and/or module fabrication could potentially be realized during production, fabrication or construction and may impact plant deployment cost and schedule. |

| ● | Our Demonstration Plant and future facilities and operations could be damaged or otherwise adversely affected as a result of natural disasters and other catastrophic events, and such adverse effects would negatively impact our ability to develop key process equipment and technologies within our anticipated timeline and budget. |

| ● | If we cannot extend the lease for our Demonstration Plant, which is currently set to expire in 2025, then we may need to remove, rebuild and relocate our equipment to a suitable facility elsewhere and resume development activities thereafter. |

| ● | The Demonstration Plant has not yet overcome all power loads to provide net positive power delivery to the commercial grid during its operation. |

| ● | We may encounter difficulty in attracting licensees prior to the deployment of an initial full-scale commercial plant. |

vi

| ● | We expect a consortium led by NET Power to undertake the first commercial plant deployment to establish our technology. Such a deployment will require significant capital expenditures. |

| ● | Our future growth and success depend on our ability to license to customers and their ability to secure suitable sites. We have not yet entered into a binding contract with a customer to license the NET Power Cycle, and we may not be able to do so. |

| ● | Conflicts of interest may arise because several directors on the Board are designated by certain of our largest stockholders. |

| ● | The energy market continues to evolve and is highly competitive. The development and adoption of competing technology could materially and adversely affect our ability to license our technology. |

| ● | The market for power plants implementing the NET Power Cycle is not yet established and may not achieve the growth potential we expect and may grow more slowly than we expect. |

| ● | There is limited infrastructure to efficiently transport and store carbon dioxide, which may limit deployment of the NET Power Cycle. |

| ● | The cost of electricity generated from the NET Power Cycle may not be cost competitive with other electricity generation sources in some markets. |

| ● | Our business relies on the deployment of power plants that are subject to a wide variety of extensive and evolving government laws and regulations, including environmental laws and regulations. |

| ● | We and our potential licensees may encounter substantial delays in the design, manufacture, regulatory approval and launch of power plants. Regulatory approvals and permits may also be denied. |

| ● | Any potential changes or reductions in available government incentives promoting greenhouse gas emissions projects, such as the Inflation Reduction Act of 2022’s financial assistance program funding installation of zero-emission technology, may adversely affect our ability to grow our business. |

| ● | We and our customers operate in a politically sensitive environment, and the public perception of fossil fuel derived energy can affect our customers and us. Our future growth and success are dependent upon consumers’ willingness to develop natural-gas-fueled power generation facilities. |

| ● | The ability to license and deploy natural gas power plants may be limited due to conflict, war or other political disagreements between gas-producing nations and potential customers, and such disagreements may adversely impact our business plan. |

| ● | We are developing NET Power-owned intellectual property, but we rely heavily on the intellectual property we have in-licensed and that is core to the NET Power Cycle. The ability to protect these patents, patent applications, and other proprietary rights may be challenged or may be faced with our inability or failure to obtain, maintain, protect, defend and enforce. |

| ● | We may lose our rights to some or all of the core intellectual property that is in-licensed by way of either the licensor not paying renewal fees or maintenance fees, or by way of third parties challenging the validity of the intellectual property, thereby resulting in competitors easily entering into the same market and decreasing the revenue that we receive from our customers. |

| ● | Our patent applications may not result in issued patents and our patent rights may be contested, circumvented, invalidated or limited in scope, any of which could have a material adverse effect on our ability to prevent others from interfering with commercialization of our technology. |

| ● | The information technology systems and data that we maintain may be subject to intentional or inadvertent disruption or other security incidents that could result in regulatory investigations or actions, litigation, fines and penalties, disruptions of our business operations, reputational harm, and other adverse business consequences. |

vii

Overview

NET Power is a clean energy technology company that has developed a novel power generation system (which we refer to as the “NET Power Cycle”) designed to produce clean, reliable and low-cost electricity from natural gas while capturing virtually all atmospheric emissions. Old NET Power was founded in 2010 and methodically progressed the technology from a theoretical concept to reality with the construction and commissioning of the Company’s demonstration facility in La Porte, Texas (the “Demonstration Plant”). The NET Power Cycle is designed to inherently capture CO2 while producing virtually no air pollutants such as SOX, NOX, and other particulates. It is nearly immune to differences in altitude, humidity and temperature and can be a net water producer rather than consumer, which can facilitate project siting and operation in a variety of climates. It can operate as a traditional baseload power plant, providing reliable electricity to the grid at capacity factors targeted to be above 90%. It can also complement intermittent renewables, providing clean dispatchable electricity that can be programmed on demand at the request of power grid operators and according to market needs, while demonstrating substantial improvements in effectiveness, affordability and environmental performance as compared to existing carbon capture technologies for power generation. It leverages existing natural gas infrastructure and avoids issues of generation capacity and grid transmission overbuild created by other technologies, helping to further reduce system-wide decarbonization costs.

The NET Power Cycle is designed to achieve clean, reliable and low-cost electricity generation through NET Power’s patented highly recuperative oxy-combustion process. This process involves the combination of two technologies:

| ● | Oxy-combustion, a clean heat generation process in which fuel is mixed with oxygen such that the resulting byproducts from combustion consist of only water and pure CO2; and |

| ● | Supercritical CO2 power cycle, a closed or semi-closed loop process that replaces the air or steam used in most power cycles with recirculating CO2 at high pressure, as sCO2, producing power by expanding sCO2 continuously through a turbo expander. |

In the NET Power Cycle, CO2 produced in oxy-combustion is immediately captured in a sCO2 cycle that produces electricity. As CO2 is added through oxy-combustion and recirculated, excess captured CO2 is siphoned from the cycle at high purity for export to permanent storage or utilization.

The NET Power Cycle was first demonstrated at our 50 MWth Demonstration Plant in La Porte, Texas, which broke ground in 2016 and began testing in 2018. We conducted three testing campaigns over three years and synchronized to the Texas grid in the fall of 2021. Through these tests, we achieved technology validation, reached critical operational milestones, and accumulated over 1,500 hours of total facility runtime as of December 31, 2023.

NET Power plans to license its technology through offering plant designs ranging from industrial-scale configurations between 25-115 MW net electric output to utility-scale units of up to 300 MW net electric output capacity. This technology is supported by a portfolio of 447 issued patents (as of December 31, 2023) in-licensed on an exclusive, irrevocable basis (in the applicable field) from 8 Rivers as well as significant know-how and trade secrets generated through experience at the Demonstration Plant. NET Power’s first-generation utility-scale design (which we refer to as Gen1U) will be a 300 MWe class power plant, targeting a CO2 capture rate of 97% or greater. Early Gen1U deployments are focused on ensuring a clean and reliable system. Based on the Company’s work to date, NET Power expects these early projects to target a net efficiency of approximately 45%. Incorporating the lessons learned from early plants’ operations, NET Power targets delivery of later Gen1U plants with net efficiency of approximately 50%.

Over the next several years, NET Power plans to conduct additional research and equipment validation testing campaigns at its Demonstration Plant and construct its first utility-scale plant. NET Power will begin purchasing initial long-lead materials for the first utility-scale plant in 2024 and targets initial power generation between the second half of 2027 and the first half of 2028. NET Power intends to deploy its technology in the United States (“U.S.”) and around the world by leveraging experience gained from the Demonstration Plant as well as from the support and expertise of NET Power’s current owners, including OXY, BHES, Constellation and SK Group.

NET Power’s potential customers include electric utilities, oil and gas companies, midstream oil and gas companies, technology companies, and industrial facilities, both in domestic and international markets. NET Power has engaged in active dialogue with potential customers in each of these industries. NET Power’s end-markets can be broken down into three general categories: baseload generation, dispatchable generation and industrial applications. Baseload generation includes replacing emitting fossil fuel-fired facilities (brownfield) or installing new clean baseload capacity (greenfield). NET Power believes many customers will seek its dispatchable technology to balance the intermittency of renewable generation. Potential industrial customers, such as direct air capture facilities, steel facilities, chemical plants, and hydrogen production facilities, include those that have significant 24-hour energy needs and goals to decarbonize. NET Power’s technology can provide the necessary clean, reliable, low-cost electricity and heat energy to these facilities as well.

1

Key benefits for customers include the following:

| ● | Clean—The NET Power Cycle is expected to result in a life cycle carbon intensity (“CI”) of 40g to 75g CO2e/kWh and capture CO2 at > 97% rate, providing for approximately 85% CO2 emissions reduction in comparison to conventional combined cycle gas turbine technology. CO2 is inherently captured at pipeline pressure and ready for transportation. The NET Power Cycle results in de minimis NOX, SOX and particulate emissions that result from traditional coal or natural gas fossil fuel generation, which may allow for project siting near population centers. NET Power expects efforts to reduce upstream methane emissions will further reduce the NET Power Cycle CI. |

| ● | Reliable—The NET Power Cycle can provide 24/7 baseload power, with a targeted capacity factor of 92.5%, power ramp rates of 10% to 15% per minute and 0% to 100% load following capabilities. It can function as a utility-scale large plant or seamlessly pair as a load-following asset to support variable renewable energy. |

| ● | Low-cost— NET Power targets levelized cost of energy in the U.S. that is lower than both legacy firm generation technology like combined cycle gas turbine and intermittent technologies such as solar photovoltaic panels (“PVs”) coupled with four hours or more of battery storage. |

| ● | Utilizes existing infrastructure—The U.S. alone has approximately 2.5 million miles of natural gas pipeline infrastructure, with over 300,000 miles of transmission pipelines. Approximately 50 individual CO2 pipelines with a combined length of over 4,500 miles exist in the U.S. today. According to the U.S. Energy Information Administration (the “EIA”), there further exist hundreds of thermal power generation facilities at or nearing their retirement or replacement period through 2050, which NET Power believes could serve as potential brownfield site locations. The EIA estimates nearly a quarter of the 200 GW of coal-fired capacity will retire by the end of 2029. Their transmission interconnections and auxiliary systems can be repurposed with minimal changes to serve NET Power’s facilities. With the addition of CO2 infrastructure, NET Power can fit within the existing grid network with low incremental cost. |

| ● | Compact footprint—NET Power’s modular design and the inherent energy density of sCO2 as a working fluid leads to a low surface footprint targeted to be less than 15 acres, equal to 1/100th of the solar PV of a similar electric output. This footprint is smaller than existing unabated combined cycle facilities of similar capacity, allowing NET Power to serve as a re-powering option for retiring facilities or facilities that cannot secure additional space for capture equipment. |

NET Power believes that the NET Power Cycle can serve as a key enabling platform for a low-carbon future, addressing shortfalls inherent to alternative options while contributing to an overall lower system-wide cost of decarbonization. NET Power believes that through its innovative process, it can provide a lower cost of electricity, reduction and in some cases elimination of environmental impacts related to thermal power use (air pollution, water use, land use and deforestation), reliability and dispatchability contributing to energy security and lower costs as well as an ability to achieve required carbon reduction targets. NET Power believes the build-out of the NET Power Cycle will provide the world with clean, reliable and low-cost energy.

Corporate Strategy

NET Power employs a three-pillar corporate strategy as the foundation to direct our capital allocation and align our decision-making with our long-term vision.

Pillar 1: Develop and prove NET Power’s technology at the utility-scale

Our first priority is to progress our joint development program with Baker Hughes. Together with Baker Hughes, we plan on conducting several testing campaigns at our Demonstration Plant in 2024 through 2026, which will provide invaluable operational data ahead of deploying our first utility-scale plant.

Concurrently, we are progressing project development of our first utility-scale plant in west Texas, including front end engineering and design (“FEED”), preparing and filing permits and interconnect applications and securing land and supply and offtake agreements. The ultimate goal for the first utility-scale deployment will be to construct and operate with a focus on clean, reliable and safe operations as we expect it to serve as the launch-point for all future deployments.

2

Pillar 2: Build the project backlog

In parallel to developing and proving NET Power’s technology, we will focus over the next few years on creating a backlog for future deployment. This involves identifying CO2 sequestration sites, securing surface rights for plant sites, filing applications to connect to the regional grid systems, and forming strategic partnerships with a variety of stakeholders to set up projects for success. With this approach, we believe we will accelerate deployment of NET Power’s technology in the most cost effective and responsible manner for the benefit of our customers, the communities where these plants will be located, and our owners. Our goal is to have a robust backlog that creates pathways to several hub deployments by the time our first utility-scale plant comes online.

Pillar 3: Prepare for manufacturing mode

One of the largest drivers of our plant economics is the plant capital cost. To reduce capital cost, NET Power plans to standardize the design, supply, and construction of NET Power plants, allowing our original equipment manufacturers and Engineering, Procurement and Construction (“EPC”) partners to enter mass manufacturing mode. Rather than each plant being bespoke with different parts sourced one-off, a standardized design means continuously producing the same parts over and over. We expect standardization and scale efficiencies will be large drivers of future capital expenditure reductions. Similarly, we expect more work will take place in a controlled factory environment, and less will take place in the field at remote locations. By taking this approach, we expect to have more control over driving down the plant capital cost, reducing project risk, and reducing lead time to build future plants.

The Business Combination

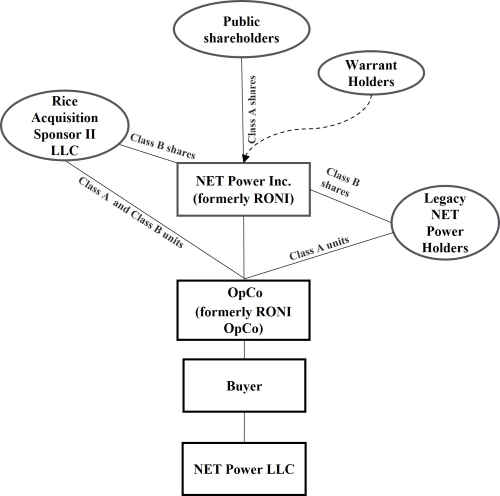

On December 13, 2022, Old NET Power entered into the Business Combination Agreement with RONI (a blank check company incorporated as a Cayman Islands exempted company on February 2, 2021 and formed for the purpose of effecting a merger, share exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more target businesses), RONI OpCo (a majority owned and controlled operating subsidiary of RONI), Buyer (a direct, wholly owned subsidiary of RONI OpCo) and Merger Sub (a direct, wholly owned subsidiary of the Buyer). On June 8, 2023, the Business Combination was consummated and, among other things, Merger Sub merged with and into Old NET Power (which we refer to as the Merger), with Old NET Power surviving the Merger.

Immediately prior to the consummation of the Merger, on June 8, 2023, as contemplated by the Business Combination Agreement, RONI became a Delaware corporation named “NET Power Inc.,” and (i) each issued and outstanding Class A ordinary share, par value $0.0001 per share, of RONI (the “Class A Shares”) was automatically converted, on a one-for-one basis, into a share of Class A Common Stock of NET Power Inc., (ii) each issued and outstanding Class B ordinary share, par value $0.0001 per share, of RONI was automatically converted, on a one-for-one basis, into a share of Class B Common Stock of NET Power Inc., and (iii) each issued and outstanding warrant of RONI (which was exercisable for a Class A Share) automatically converted into a warrant to purchase one share of Class A Common Stock of NET Power Inc. Immediately following this Domestication, RONI OpCo became a Delaware limited liability company and was renamed NET Power Operations LLC.

3

Following such Domestications, the Merger was consummated, and at the effective time of the Merger, the issued and outstanding equity interests of Old NET Power were canceled and converted into the right to receive an aggregate of 137,192,563 Class A units of OpCo and an equivalent number of shares of Class B Common Stock. The OpCo LLC Agreement provides each member of OpCo (other than the Company) the right to cause the Company to cause OpCo to redeem all or a portion of such member’s Class A units of OpCo in exchange for an equal number of shares of Class A Common Stock or, at the Company’s election under certain circumstances set forth therein, cash, in each case, subject to certain restrictions set forth therein. Upon redemption of any OpCo Units, an equal number of shares of Class B Common Stock held by the redeeming member of OpCo is canceled.

Also on June 8, 2023, in connection with the consummation of the Merger, the Company consummated the private placement of 54,044,995 shares of Class A Common Stock for gross proceeds of $540,449,950 (the “PIPE Financing”).

Government and Regulatory Environment

Carbon-free energy technology has received significant support in the last several years at the U.S. federal level, with valuable improvements to existing tax credits, new grant appropriations, and additional loan guarantee authority.

Grant and Loan Opportunities—The November 2021 Bipartisan Infrastructure Law (“BIL/IIJA”) provided further support to the DOE Loan Program Office (“LPO”) Title XVII program to support early commercial facilities across the U.S. More recently, the Inflation Reduction Act (the “IRA”), which was adopted in August 2022, ushered in further support to LPO Title XVII (additional appropriations of $40 billion through 2026), $3.6 billion to cover credit subsidy costs of loans and introduced a new “Energy Infrastructure Reinvestment” fund with $250 billion of new commitment authority to “retool, repower, repurpose, or replace energy infrastructure” with emission control technologies.

Global funding opportunities, such as the European Union (“EU”) Innovation Fund, the European Commission’s Just Transition Fund, and the United Kingdom (“UK”) Department for Business, Energy & Industrial Strategy (“BEIS”) Net Zero Innovation Portfolio, offer opportunities in Europe. Other opportunities exist across the world, and we are evaluating these on a case-by-case basis to de-risk and support initial projects.

4

Tax Credit Opportunities—The IRA also provided dramatic enhancement to the 45Q tax credit program, a tax credit providing incentives to CO2 capture facilities. It increased the credit value per metric ton of captured CO2 from $50 to $85/ton of CO2 permanently geologically sequestered, with similar enhancements allocated to CO2 captured and then utilized for enhanced oil recovery (“EOR”) or other uses, from $35 to $60/ton CO2. Further changes to the regulations improved the 45Q tax credit opportunity through the relaxing of program restrictions, reducing the annual CO2 capture threshold to qualify for the credit, providing a multi-year extension on the commencement of construction window, allowing for “direct pay” for the first five years after carbon capture is placed in service, and creating a “design” minimum capture rate for electric generating units of 75%, which the NET Power Cycle is inherently designed to meet and exceed.

We are monitoring the global market for other tax credit or carbon tax opportunities, with the belief that any value ascribed to carbon, whether a credit or tax, benefits our technology over other emitting alternatives.

NET Power Cycle Licenses and Support Services

In the future, our primary revenue stream is expected to be license and royalty fees paid by the customer for each project. A customer seeking to deploy a NET Power plant will purchase a license from us to construct, operate, and maintain the plant. We expect that the customer will pay a license deposit before the commencement of FEED, which would be credited toward the license fee, and the remaining license fee would be paid in installments at key milestones leading to a plant’s commercial operations. We also expect that customers will pay an annual royalty fee for the life of the plant. We currently expect each 300 MWe class license to generate discounted present value licensing fees of approximately $65 million using a 10 percent discount rate.

In addition to licenses, we expect to provide customers with a list of pre-qualified EPC companies. We believe that our pre-qualification of these EPC companies can provide customers with reasonable confidence that the contractors they engage have the requisite skill and expertise to successfully deliver a NET Power plant. Furthermore, this process is designed to ensure that EPC companies understand and appreciate our business model and quality control expectations.

We expect to also provide customers with a preferred vendors list and a robust approved list for key equipment suppliers, further ensuring quality control and de-risking the supply chain. Customers developing a NET Power plant will purchase equipment from one of our licensed suppliers.

We intend to provide support to customers throughout the development process. During scoping and early development of potential facility sites, we will conduct feasibility studies and pre-FEED for customers. When customers are ready to begin FEED processes, we intend to provide a license package with the necessary specifications to pre-qualified EPC companies. We plan to support each customer’s execution of FEED, with the appropriate scope of work being determined on a case-by-case basis. We expect that our support will continue to the commercial operations of each plant and will include support for start-up and commissioning as well as operator training.

We also intend to originate and develop early projects by identifying sites, securing land and sequestration rights, filing interconnection and sequestration permit applications, and securing supply and offtake agreements. We intend to partner with local businesses in the regions we originate projects, and expect the originated projects to pay us license and royalty fees similar to those paid by third-party customers.

Competition

Our competitors are other power generation technologies, including traditional baseload, renewables, and advanced nuclear. We believe our competitive strengths differentiate us from our competition globally, in part because we expect our technology to achieve clean, reliable, and low-cost power generation while we expect most of our competitors only achieve two of these three factors.

Traditional Baseload—According to the International Energy Agency (the “IEA”), approximately 72% of global generation capacity in 2020 was natural gas, coal, oil and large-scale nuclear. These technologies are highly reliable, cost-effective and dispatchable. However, with the exception of traditional large-scale nuclear, these resources are carbon-intensive, and we expect them to largely be replaced with carbon-free generation over time. Traditional natural gas power plants, while delivering lower carbon electricity than other fossil fuel feedstocks, are not viewed as a permanent solution by certain regulators and policymakers in light of concerns related to climate change. Instead, some view conventional natural gas as a bridge fuel until other sources of energy are available. Our technology combines the reliability of natural gas with the decarbonizing capabilities of carbon capture.

5

Advanced Nuclear—There are several advanced nuclear reactor technologies that are in various stages of development. These technologies are designed to be clean, safe and highly reliable. However, these technologies have not received regulatory approval in the U.S., and many of the technologies have not been demonstrated and generally do not have fuel supply infrastructure in existence. As of December 31, 2023, there is only one small modular reactor (“SMR”) that has received a Standard Design Approval from the U.S. Nuclear Regulatory Commission, and while Standard Design Approvals are not required for SMR designs, alternative regulatory pathways for permitting and constructing SMRs also entail substantial uncertainties with respect to cost and timing.

Renewables—According to the IEA, approximately 28% of global generation capacity in 2020 was wind, solar, hydroelectric and other renewable power generation sources. Although these sources generate carbon-free power, wind and solar can be intermittent and non-dispatchable, unless paired with storage, and hydroelectric can be seasonal and, subject to curtailment. Additionally, since renewables are weather-dependent, we believe they are too unreliable to support certain end-use cases, including certain mission-critical applications or industrial applications that require extensive on-site, always-available power. Our technology allows for the reliability and low-cost nature of natural gas to remain intact while reducing carbon emissions arising from natural gas-fired generation of electricity.

Customers

Our potential customers include electric utilities, independent power producers, oil and gas companies, midstream companies, renewable energy companies, clean energy technology companies, and industrial facilities, both in domestic and international markets. Our end-markets can be broken down into three general categories: baseload generation, dispatchable generation, and industrial applications. Baseload generation includes the replacement of emitting fossil fuel-fired facilities or the installation of new clean baseload capacity. Some customers may deploy the facility to provide a reliable low-cost energy source to complement intermittent renewables, helping the grid reduce carbon emissions. Potential industrial customers, such as direct air capture facilities, steel facilities, chemical plants, and hydrogen production facilities, include those that have significant energy needs and goals to decarbonize. Our technology can provide the necessary clean, reliable electricity and heat energy to these facilities.

Partnerships

License Agreement with 8 Rivers

On August 7, 2014, we entered into a license agreement with 8 Rivers, pursuant to which 8 Rivers granted us perpetual, irrevocable worldwide rights under patents relating to the NET Power Cycle (which was invented by 8 Rivers), for the generation of electricity using CO2 as the primary working fluid. The license is exclusive in the field of utilizing any carbonaceous gas fuel other than those derived from certain solid fuel sources. 8 Rivers remains an investor in us.

License Agreement and Joint Development Agreement with Baker Hughes

On February 3, 2022, we entered into the Original JDA, which was amended and restated on December 13, 2022. Pursuant to this agreement, NPI is developing sCO2 turbo expanders for use in facilities implementing the NET Power Cycle. These turbo expanders are intended to be compatible with our existing technology and are highly specialized. We and NPI formed a Joint Design Committee to provide oversight and support for program schedule, equipment design and performance.

NPI will oversee the installation and commissioning of the first industrial scale combustor and turbo expander at the Demonstration Plant. A team of NPI specialists will be deployed at the site offering technical advice and conducting testing and validation processes. We intend to work with NPI to ensure the implementation and integration process occurs according to plan and any required personnel is trained properly.

In connection with the Original JDA, on February 3, 2022, NET Power entered into the BH License Agreement with NPT (the “BH License Agreement”), pursuant to which NPT and its affiliates will have limited exclusivity for manufacturing utility-scale turbo expanders and full exclusivity for industrial-scale units. We will own intellectual property developed by NPI related to the NET Power Cycle, and NPI can only sell the jointly developed turbo expanders to our licensees. We and NPI will market through a Joint Commercial Committee, leveraging Baker Hughes’ global sales channels.

6

OLCV NET Power, LLC Investment

OXY invested in NET Power in 2019 and provides expertise in the CO2 value chain. OXY is expected to play a key role in the development and commercialization of the first utility-scale NET Power plant (“Serial Number 1”) and will provide the host site for the project near Odessa, Texas.

Intellectual Property

As of December 31, 2023, our technology is supported by a portfolio of 447 issued patents (and 67 pending applications) that extends across more than 30 countries and six continents. These patent rights have been in-licensed from 8 Rivers pursuant to a 2014 license agreement which provides us with exclusive licensing, sublicensing and commercialization rights for natural gas and certain other fuel sources. Such patents extend through the mid-2030s. Protections are intended to provide coverage for integrated permutations of the patented technology as it expands as a platform and not simply a power generation concept. We also have trade secrets that may provide for an additional scope of protected and licensable rights extending beyond patent lifetimes.

Our intellectual property encompasses rights under patents related to the NET Power Cycle and trade secret information derived from the Demonstration Plant. Our registered trademarks include the NET Power logo and company name. We also have explicit company policy to protect our proprietary data through various classification, handling, and control systems.

Pursuant to the BH License Agreement, NPT and its affiliates will have limited exclusivity for manufacturing utility-scale turbo expanders and full exclusivity for industrial-scale units. We will own intellectual property developed by NPI related to the NET Power Cycle, and NPI can only sell the jointly developed turbo expanders to our licensees. The Amended and Restated JDA and the BH License Agreement include contractual obligations dictating the use of our intellectual property to preserve its integrity.

Our technology, including its use and incorporation in processes, plants, and components for use, is protected by certain intellectual property and contractual rights in the U.S. and various other countries of the world. We continually review our development efforts to assess the existence and patentability of our intellectual property. Our intellectual property continues to grow and expand, protecting iterative product design and development of our technology.

We rely upon a combination of patents, copyrights, trade secrets and trademark laws, along with employee and third-party non-disclosure agreements and other contractual restrictions to establish and protect our proprietary rights. Patent protection was obtained shortly after the invention of our technology, providing protection for this one-of-a-kind natural gas cycle from its earliest stages.

Human Capital

As of December 31, 2023, we had 43 full-time employees and four contractors and on-site service employees. Our headquarters are located in Durham, North Carolina and we also anticipate opening a Houston office by the middle of 2024. None of our employees are subject to a collective bargaining agreement. We consider our relationship with our employees to be positive.

Talent Acquisition and Retention

We support business growth by seeking to attract and retain best-in-class talent. We use internal and external resources to recruit highly skilled candidates for open positions. We provide employees with compensation packages that may include various components, such as base salary, annual incentive bonuses and long-term equity incentive awards. We also offer comprehensive employee benefits, such as life, disability and health insurance, vision and dental insurance, paid time off, and a 401(k) plan with an employer contribution. It is our intention to be an employer of choice in our industry by providing a market-competitive compensation and benefits package.

Training and Development

We believe in encouraging employees to become lifelong learners by providing ongoing learning and leadership training opportunities. While we strive to provide real-time recognition of employee performance, we have a formal annual review process designed to identify areas where training and development may be necessary or beneficial.

7

Diversity, Equity, Inclusion & Accessibility

We believe a diverse workforce is critical to our success. Our mission is to value differences in races, ethnicities, religions, nationalities, genders, ages, abilities and sexual orientations as well as education, skill sets and experience. We are focused on inclusive hiring practices, fair and equitable treatment, organizational flexibility and training and resources.

Government Regulations

Energy Regulatory Matters

Electric power sales and markets in the U.S. are subject to extensive regulation at both the federal and state levels. Accordingly, NET Power’s Demonstration Plant, which is located within the Electric Reliability Council of Texas (“ERCOT”), and other NET Power plants that NET Power may own in the future located in ERCOT and other jurisdictions within the U.S. are subject to substantial energy regulation and may be adversely affected by legislative or regulatory changes, as well as liability under, or any future ability to comply with, existing or future energy regulations or requirements. Compliance with the requirements under these various regulatory regimes may cause the applicable company to incur significant costs, and failure to comply with such requirements could result in the shutdown of the non-complying facility or the imposition of liens, fines, or civil or criminal liability.

State regulators also regulate the rates that retail utilities can charge and the terms under which they serve retail (end-use) electric customers. Certain states also have authority to regulate mergers, acquisitions, financing, and securities issuances. State regulators may also review individual utilities’ electricity supply requirements and have oversight over the ability of traditional regulated utilities to pass through to their ratepayers the costs associated with power purchases from independent generators. Federal regulatory filings and authorizations generally are required for generation projects in the U.S. that sell energy wholesale and are connected to the interstate transmission grid. Furthermore, even when a particular energy business entity is subject to federal energy regulation, state and local approvals (such as siting and permitting approvals) are often required.

Federal Power Act

The Federal Power Act (the “FPA”) provides the Federal Energy Regulatory Commission (“FERC”) exclusive federal jurisdiction over the sale of electric energy at wholesale (that is, for resale) in interstate commerce and the transmission of electric energy in interstate commerce, including wholesale markets for electric energy, capacity, ancillary services, and transmission services. Section 205 of the FPA gives FERC jurisdiction includes, among other things, authority over the rates, charges, and other terms for the sale of electric energy, capacity, and ancillary services at wholesale by public utilities (entities that own or operate projects subject to FERC jurisdiction) and for transmission services. These rates may be based on a cost-of-service approach or may be determined on a market basis through competitive bidding or negotiation. As a result, a public utility must obtain FERC approval of its rates and charges and must make the associated, required filings to maintain the granted authority. To obtain authority to make sales at market-based rates, the public utility must demonstrate to FERC that it does not possess market power, as defined by FERC.

The FPA also provides FERC authority for the regulation of mergers, acquisitions, financings, and securities issuances involving entities subject to its jurisdiction. In certain cases, FERC approval may be required prior to entering into a transaction involving a public utility.

ISOs and RTOs

Generation projects also may be located in regions in which the bulk power transmission system and associated wholesale markets for electric energy, capacity, and ancillary services are administered by Independent System Operators (“ISOs”) and Regional Transmission Organizations (“RTOs”) that are subject to FERC jurisdiction and operate under FERC jurisdictional tariffs, including open access transmission tariffs, or, in the case of ERCOT, generation, and transmission tariffs and protocols that are regulated by the PUCT. These RTOs and ISOs prescribe rules and protocols for the terms of participation in the wholesale energy and ancillary services markets (and for certain RTOs and ISOs, capacity markets). Many of these entities can impose rules, restrictions, and terms of service that are regulatory in nature and may have a material adverse effect on business. For example, ISOs and RTOs have developed bid-based locational pricing rules for the electric energy markets that they administer. In addition, most ISOs and RTOs have also developed bidding, scheduling, and market behavior rules, both to curb the potential exercise of market power by electricity generating companies and to ensure certain market functions and system reliability. These rules, restrictions, and terms of service could change over time and could materially adversely affect a power plant’s ability to sell, and the price received for, energy, capacity, and ancillary services.

8

Energy Policy Act of 2005

NET Power and its projects may also be subject to the mandatory reliability standards of the North American Electric Reliability Corporation (the “NERC”). In 2005, the U.S. federal government enacted the Energy Policy Act of 2005, which supplemented the FPA to vest FERC with authority to ensure the reliability of the bulk electric system. Such authority mandated that FERC assume both oversight and enforcement roles. Pursuant to this mandate, FERC certified the NERC as the nation’s Electric Reliability Organization (“ERO”) to develop and enforce mandatory reliability standards and requirements to address medium- and long-term reliability concerns. The NERC reliability standards are a series of requirements that relate to maintaining the reliability of the North American bulk electric system and cover a wide variety of topics, including physical security and cyber-security of critical assets, information protocols, frequency and voltage standards, testing, documentation, and outage management. If generation and transmission owners and operators that are part of the bulk electric system fail to comply with these standards, they could be subject to sanctions, including substantial monetary penalties. NERC and FERC also delegate these responsibilities to regional entities, such as Texas Reliability, Inc., which enforce both NERC and regional reliability standards.

Public Utility Holding Company Act of 2005

The Public Utility Holding Company Act of 2005 (“PUHCA”) provides FERC and state regulatory commissions with access to the books and records of holding companies and other companies in holding company systems; it also provides for the review of certain costs. Companies like NET Power that are holding companies under PUHCA solely with respect to one or more Exempt Wholesale Generators or Qualifying Facilities are generally exempt from requirements which give FERC access to books and records.

State Utility Regulation

While federal law provides the utility regulatory framework for our project subsidiaries’ sales of electric energy, capacity, and ancillary services at wholesale in interstate commerce, there are also important areas in which traditional public utilities fall under state jurisdiction. For example, the regulated electric utility buyers of electricity from our projects are generally required to seek state public utility commission approval for the pass-through in retail rates of costs associated with power purchase agreements entered into with a wholesale seller or seek approval for the siting and construction of a new power plant. Certain states also regulate the acquisition, divestiture, and transfer of some wholesale power projects and financing activities by the owners of such projects. In addition, states and other local agencies require a variety of environmental and other permits.

Texas

The Demonstration Plant is located in ERCOT. ERCOT is a largely self-contained market on a standalone grid with only approximately 1,100 MW of transfer capability through direct-current, asynchronous ties with the Southwest Power Pool, and the Comision Federal de Electricidad in Mexico. Therefore, in ERCOT, the wholesale electricity market is, for most purposes, considered to be intrastate commerce, and so its rules, as well as the provision of transmission and distribution service in Texas, generally remain regulated by the Public Utility Commission of Texas (the “PUCT”).

The PUCT, with the help of ERCOT, regulates competitive market participants, including power generation companies (i.e., owners and operators of power plants that make sales into the wholesale electricity and ancillary services markets in ERCOT) and power marketers (i.e., entities that do not own power plants but make sales of electricity at wholesale). Such regulation includes oversight of operations (including imposing real-time telemetry and dispatch requirements, monitoring for market power abuses, and requiring emergency operations planning and weather preparedness), registration, reporting, and record-keeping requirements. The PUCT and ERCOT do not directly regulate wholesale or retail prices, except to monitor for potential market power abuses and anti-competitive behavior. The PUCT has authority to investigate and impose fines for violations of its enabling statute, the Public Utility Regulatory Act (Tex. Util. Code §§ 11.001-66.016), its rules (set out in Chapter 25 of Title 16 of the Texas Administrative Code), and of the ERCOT Protocols or other binding documents. Fines can be up to $25,000 per violation per day for most violations and up to $1,000,000 per violation per day for specific violations relating to weather-preparedness requirements.

Power generation companies also must seek pre-approval from the PUCT for proposed mergers, acquisitions, or other affiliations with other power generation companies in certain circumstances, pursuant to the Public Utilities Regulatory Act § 39.158.

The structure of the energy industry and its regulation in the U.S. is currently, and may continue to be, subject to change. We expect the laws and regulation applicable to our business and the energy industry generally to be in a state of transition for the foreseeable future. Changes in such laws and regulations could have a material adverse effect on our business, financial condition, and results of operations.

9

Environmental Matters

Power plant operations are required to comply with various environmental, health, and safety (“EHS”) laws and regulations. For NET Power plants in which we have an ownership interest, these existing and future laws and regulations may affect existing and new projects, require us to obtain and maintain permits and approvals, undergo environmental review processes, and implement EHS programs and procedures to monitor and control risks associated with the siting, construction, operation, and decommissioning of regulated or permitted energy assets, all of which involve a significant investment of time and resources.

We also incur costs in the ordinary course of business to comply with these laws, regulations, and permit requirements. EHS laws and regulations frequently change, and often become more stringent or subject to more stringent interpretation or enforcement over time. Such changes in EHS laws and regulations, or the interpretation or enforcement thereof, could require us to incur materially higher costs, or cause a costly interruption of operations due to delays in obtaining new or amended permits.

The failure of our project operations to comply with EHS laws and regulations, and permit requirements, may result in administrative, civil, and criminal penalties, imposition of investigatory, cleanup, and site restoration costs and liens, denial or revocation of permits or other authorizations, and issuance of injunctions to limit, suspend, or cease operations.

In addition, claims by third parties for damages to persons or property, or for injunctive relief, have been brought in the past against owners and operators of projects similar to the projects we will own and operate, as a result of alleged EHS effects associated with such projects, and we expect such claims may be brought against us in the future.

Environmental Regulation

To construct and operate our projects, we are required to obtain from federal, state, and local governmental authorities a range of environmental permits and other approvals, including those described below. In addition to being subject to these regulatory requirements, we or similar projects have experienced and/or may experience significant opposition from third parties during the permit application process or in subsequent permit appeal proceedings.

| ● | Clean Water Act. In some cases, our projects may be located near wetlands and we will be required to obtain permits under the federal Clean Water Act from the U.S. Army Corps of Engineers (the “Army Corps”) for the discharge of dredged or fill material into waters of the U.S., including wetlands and streams. The Army Corps may also require us to mitigate any loss of wetland functions and values that accompanies our activities. In addition, we are required to obtain permits under the federal Clean Water Act for water discharges, such as storm water runoff associated with construction activities, and to follow a variety of best management practices to ensure that water quality is protected and effects are minimized. |

| ● | Bureau of Land Management (“BLM”) Right-of-Way Grants. Our projects may be located, or partially located, on lands administered by the BLM. Therefore, we may be required to obtain and maintain BLM right-of-way grants for access to, or operations on, such lands. Obtaining and maintaining a grant requires that the project conduct environmental reviews (discussed below) and implement a plan of development and demonstrate compliance with the plan to protect the environment, including potentially expensive measures to protect biological, archaeological, and cultural resources encountered on the grant. |